A certificate of deposit (CD) is a product offered by banks and credit unions that provides an interest rate premium in exchange for the customer agreeing to leave a lump-sum deposit untouched for a predetermined period of time. Almost all consumer financial institutions offer them, although it’s up to each bank which CD terms it wants to offer, how much higher the rate will be compared to the bank’s savings and money market products, and what penalties it applies for early withdrawal. In cryptocurrency this process is completely decentralized and without any middleman (banks, etc..), relying completely on Smart Contracts.

How Does a CD Work?

Opening a CD on blockchain is very similar to opening any standard bank deposit account. After you’ve shopped around and identified which CD(s) you’ll open, completing the process will lock you into a three things.

The interest rate: Locked rates are a positive in that they provide a clear and predictable return on your deposit over a specific time period. The Smart Contract cannot later change the rate and therefore reduce your earnings.

The term: This is the length of time you agree to leave your funds deposited to avoid any penalty (e.g., 6-month CD, 1-year CD, 18-month CD, etc.) The term ends on the “maturity date,” when your CD has fully matured and you can withdraw your funds penalty-free.

The principal: This is the amount you agree to deposit when you open the CD.

Best CD Coins To Invest In

The Axion Network is a cryptocurrency investment platform meant for income centered investors. The token leverages smart contracts to offer predictable returns to investors based on a scenario with similarities to the traditional certificates of deposit. Axion brings new capital through daily auctions, alongside a buyback plan that builds stability and reliable inflation for stakeholders. Token infrastructure also has penalties for investors who unstake before achieving the initially agreed date of maturity. Investors who do not divest when their staking period ends are also penalized. In general, the network structure is set up to penalize unexpected sales with the potential of damaging Axion’s value.

With a high-interest time-locked savings account, participants in the Axion Network are rewarded daily. Put some Axion in a time-locked savings, and enjoy life, living off the interest!

Let’s say you stake 100 Axions and receive an additional 50 Axions as a stake in the settlement pool for a specified period of 100 days. In the event that you decide to unstake after 30 days, your percentage penalty will be 70% of the final payment (principal and interest). So you will receive only 30% of your staked asset, which is 45 Axion.

Like early withdrawals, participants are also charged a late penalty fee if they fail to unstake the staked token. In this case, the penalty will be 2% of the amount that can be requested for each week of non-participation. This penalty can continue for up to 50 weeks, until 100% of Axion tokens are confirmed to have been penalized.

All tokens collected as a penalty will be sent to the auction pool the next day. Interested participants can bid in ETH, and they can get tokens at a price that is usually cheaper than the one on exchanges.

20% of the ETH that Axion receives through this process will be used to fund network operations, while the remaining 80% will be used to buy back Axion tokens from exchanges. This will help Axion maintain inflation over token value and deliver a fixed 8% annual return for all participants.

Just as there are penalties for those unstakeers earlier than a set time, there is also a bonus program that encourages people to lock in their wealth for a previously agreed minimum stake.

This bonus will be accompanied by an 8% annual return, this date is known as Big Pay Days. Each year (365 days), the network offers about 20% bonuses and will double when the staking period passes two years or 730 days. The bonus will continue to multiply until about 1820 days (5 years). After this time there will be no bonuses.

So the longer you invest, the more money you can make without having to do anything.

Another important thing to note here is the transparency of Axion’s performance. The project founders have no equity in the network, unlike other cryptocurrencies like Bitcoin, where nearly 42% of the funds are held by a small group of large investors who have You can move the market at will to create huge profits for yourself.

HEX is an ERC-20 token that pays holders for rewards instead of miners, essentially a crypto version of a traditional fixed deposit account. Users can lock up funds, then receive their investment plus interest when the term matures.

HEX STAKES AVERAGE 40% INTEREST A YEAR, BEFORE USD APPRECIATION, WHICH FURTHER MULTIPLIES PROFIT.

HEX is the first blockchain certificate of deposit. HEX virtually lends value from stakers to non stakers, as staking reduces supply, causing positive price pressure on unstaked coins.

HEX’s USD price went up 352x in 361 days. HEX is more secure, faster, cheaper, better for the environment, has more features and addresses a larger market than Bitcoin. So far, HEX’s price went up 146x in Bitcoin.

HEX is like a notepad showing everyone’s HEX balance and requiring their passwords to spend. Shareholders profit from the 3.69% annual inflation, early & late end stake penalties.

You mint shares by time-locking HEX (staking), with bonuses of 20% per year, up to 3x for longer and 1.1x for larger. The HEX needed to create a share (share price) goes up every day or two, simulating compounding interest. HEX is easy!

Best ways to buy ETH to buy HEX with.

A. Directly in metamask via Wyre. B. Slower, but supports large amounts: Bitstamp is a good option. Coinbase, Kraken, and Gemini are OK too. C. Credit card or GBP, EUR & INR wire transfers via the widget below. (5 minute delivery possible) D. Changelly supports cards & wires.

Cryptocurrency exchanges are websites where you can buy, sell, or exchange cryptocurrencies for other digital currency or traditional currency like US dollars or Euro. For those that want to trade professionally and have access to fancy trading tools, you will likely need to use an exchange that requires you to verify your ID and open an account. If you just want to make the occasional, straightforward trade, there are also platforms that you can use that do not require an account.

Types of crypto exchanges

Trading Platforms – These are websites that connect buyers and sellers and take a fee from each transaction.

Direct Trading – These platforms offer direct person to person trading where individuals from different countries can exchange currency from their bank account. Direct trading exchanges don’t have a fixed market price, instead, each seller sets their own exchange rate.

Brokers – These are websites that anyone can visit to buy cryptocurrencies at a price set by the broker. Cryptocurrency brokers are similar to foreign exchange dealers.

What to look out for before joining crypto exchanges

It’s important to do a little homework before you start trading. Here are a few things you should check before making your first trade.

Reputation – The best way to find out about an exchange is to search through reviews from individual users and well-known industry websites. You can ask any questions you might have on forums like BitcoinTalk or Reddit.

Trading Fees – Most exchanges should have fee-related information on their websites. Before joining, make sure you understand deposit, transaction and withdrawal fees. Fees can differ substantially depending on the exchange you use.

Payment Methods – What payment methods are available on the exchange? Credit card? Debit card? Wire transfer through your bank account? PayPal? Can you trade with USD EUR? If an exchange has limited payment options then it may not be convenient for you to use it. Remember that purchasing cryptocurrencies with a credit card will always require identity verification and come with a premium price as there is a higher risk of fraud and higher transaction and processing fees. Purchasing cryptocurrency via wire transfer will take significantly longer as it takes time for banks to process.

Verification Requirements – The vast majority of the Bitcoin trading exchanges both in the US and the UK require some sort of ID verification in order to make deposits & withdrawals. Some exchanges will allow you to remain anonymous. Although verification, which can take up to a few days, might seem like a pain, it protects the exchange against all kinds of scams and money laundering.

Geographical Restrictions – Some specific user functions offered by exchanges are only accessible from certain countries. Make sure the exchange you want to join allows full access to all platform tools and functions in the country you currently live in.

Exchange Rate – Different exchanges have different rates. You will be surprised how much you can save if you shop around. It’s not uncommon for rates to fluctuate up to 10% and even higher in some instances.

Which crypto exchanges are best to buy bitcoin?

FTX Exchange ($FTT Token) is a leveraged cryptocurrency trading platform offering derivatives trading. The key advantage of FTX is that it built by professional traders “Alameda research” – a quant trading firm that is responsible for 30% of the market trading volume on major exchanges. FTX offers innovative products not found on other exchanges such as MOVE indices that track the volatility of cryptocurrencies and leveraged tokens (such as the 3XBULL tokens) which are long positions represented by ERC-20 tokens. In this review, we’ll explain the products on offer and how to use FTX exchange. In addition, we’ll look at the platform safety measures such as liquidation & clawback protection. Finally, we’ll look at the FTX trading fees and trading discounts (such as the $FTT native platform token).

If your focus is to conduct crypto-to-crypto trading, Binance is one of the best options. Ranked as one of the most popular cryptocurrency exchanges worldwide, they provide you with impressive offerings along with an extremely low trading fee. Although the Binance platform is a young entrant into the market, it is rapidly growing, and holds a huge selection of altcoins with Bitcoin, Ethereum, and Tether pairings.

The exchange offers its own coin termed as BNB (Binance coin). Being a centralized exchange, you can get decent discounts while conducting trade with their token. Binance offers a standard trading fee of only 0.1% which can even be reduced further if the payment is made with in BNB.

Public blockchain cryptocurrencies such as Bitcoin are radically transparent at the protocol level: transactions are viewable and immutable to everyone forever on the blockchain ledger. They are not anonymous, but rather are pseudonymous, like email addresses. And just as a person can opt to use extra privacy-preserving techniques for email, cryptocurrency users can adopt special cryptographic technologies to secure more privacy for themselves.

This explainer will describe a few of the most popular privacy-preserving techniques in the cryptocurrency space and will explain how they work. As we will see, there are multiple ways to achieve extra privacy with cryptocurrency transactions, and many reasons why users might want to adopt these methods.

The computing challenge, in a nutshell

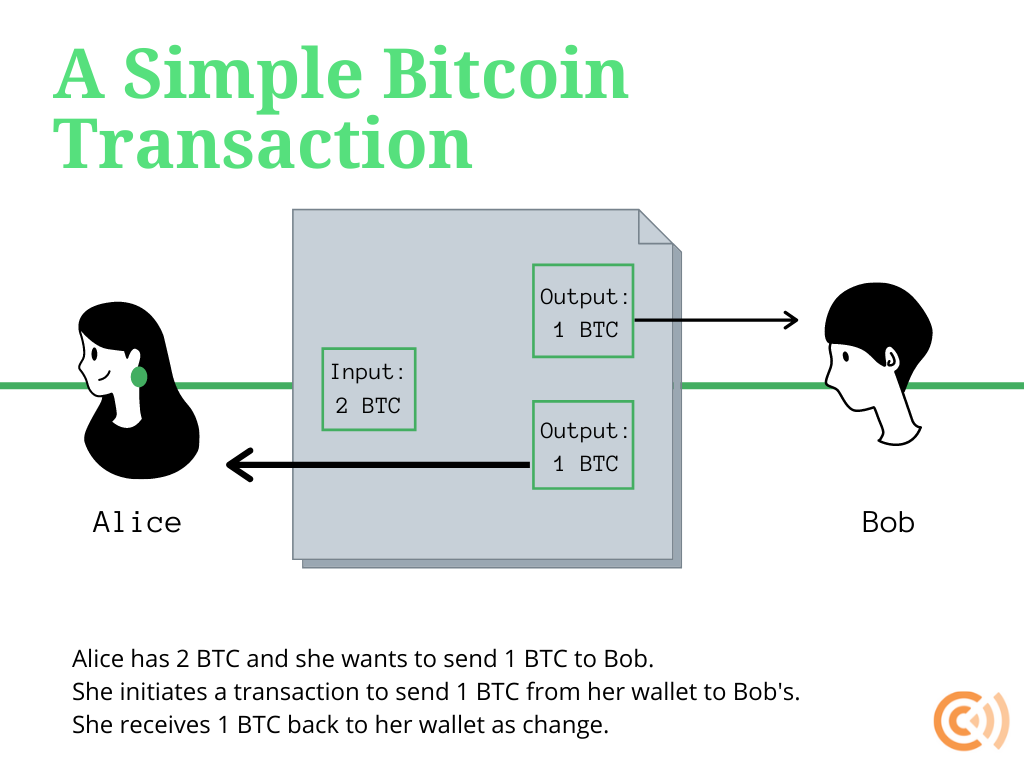

Bitcoin and similar cryptocurrency transactions are made up of one or more specified currency amount inputs (to the recipient) and one or more specified currency amount outputs (from the sender) at a certain time, all of which are recorded on the blockchain as what is called an “unspent transaction output” (UTXO). Each input was at one point the output of a previous transaction. The aggregated linkages of inputs and outputs can be traced using blockchain analysis programs.

Although users can create as many addresses to send or receive transactions as they would like, if they are not careful, they can easily leak data to uninvolved parties. Depending on how the transaction is structured, through blockchain forensics it may be possible to unmask the identity of the sender, recipient, or both, along with the amount of money sent.

For example, let’s say that a user displays a public address on his personal webpage to solicit cryptocurrency donations from supporters. He lives under a repressive government that does not grant freedom of the press. If that user sends cryptocurrency from his identity-linked address to a newly-created address to purchase a censored newspaper subscription, the government could trace that transaction back to his identity-linked address and punish him.

Here is another example. Let’s say that a non-governmental organization exists to help people living under repressive regimes. The NGO uses cryptocurrency to help fund dissidents in their activities. A repressive government can look at the transactions emanating from the NGO’s address to hunt down activists.

Individuals who wish to maintain privacy should not structure their transactions as described above. They can employ one of many privacy-preserving techniques for cryptocurrency transactions that have been developed to shield the sender, recipient, or amounts involved, or some combination of these, from unrelated observers. This can be done through mixers, CoinJoins, or protocol-level features of certain privacy-preserving cryptocurrencies.

Mixers and CoinJoins

There are two broad techniques to attain more privacy with Bitcoin transactions. A user can seek out a “mixer” service, which is generally offered by a third-party custodian, or undertake a “CoinJoin” transaction, which is always non-custodial.

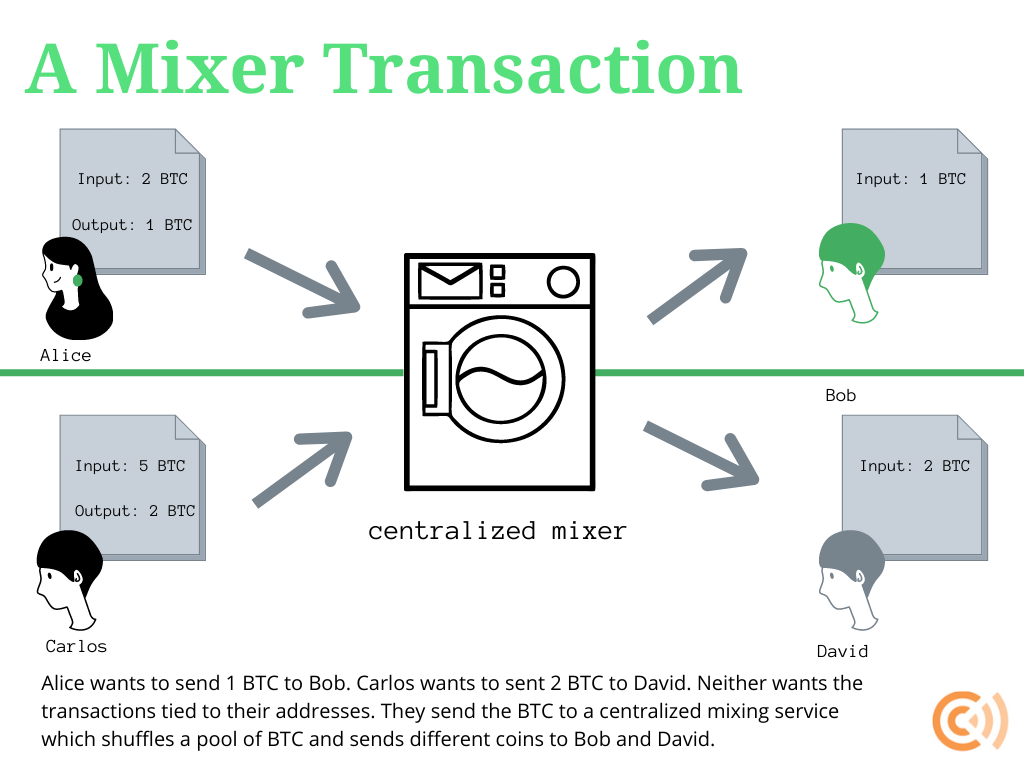

Mixers, also known as “tumblers,” were one early Bitcoin privacy technique. The process is straightforward: privacy-seeking cryptocurrency users would send transactions to a mixer service which, in exchange for a fee, would then “mix” the pool of cryptocurrency together to de-link the transaction trail.

Initially, mixer services were only offered by third parties, which had to be trusted. This centralization means that mixer users are at the mercy of service providers. A dishonest mixer could secretly keep records of transactions or poorly mix the coins. In the extreme case, a mixer could simply abscond with the money.

But simple centralized mixing has a huge downside even when mixers are perfectly honest and capable: non-criminal mixer users may receive coins that are tainted by criminals that use that same mixing service. In other words, although privacy may be more preserved with a simple centralized mixer, a non-criminal user may still receive coins with a “taint” of someone else’s crime. Because receiving tainted coins is undesirable, this creates a problem of imperfect fungibility since untainted coins may be worth more than tainted coins.

Improvements to this model were eventually made. For example, a “smart pool” mixer combines user-submitted funds, which might include the proceeds of a criminal act, with private reserves from the mixer and investors, which are unlikely to have been associated with any crime. A “stealth pool” takes this logic even further, completely separating user-submitted coins from reserve and investor coins that are paid out to new addresses; in other words, there is little chance that a user will receive tainted coins. Mixing services may also delay payments over a set period of time or spread out payments among separate wallets to further obfuscate the trail.

Eventually, more peer-to-peer methods to preserve privacy were developed. These achieve a similar end to centralized mixing—namely, concealing transaction senders, recipients, or amounts or some combination of these—with fewer of the downsides.

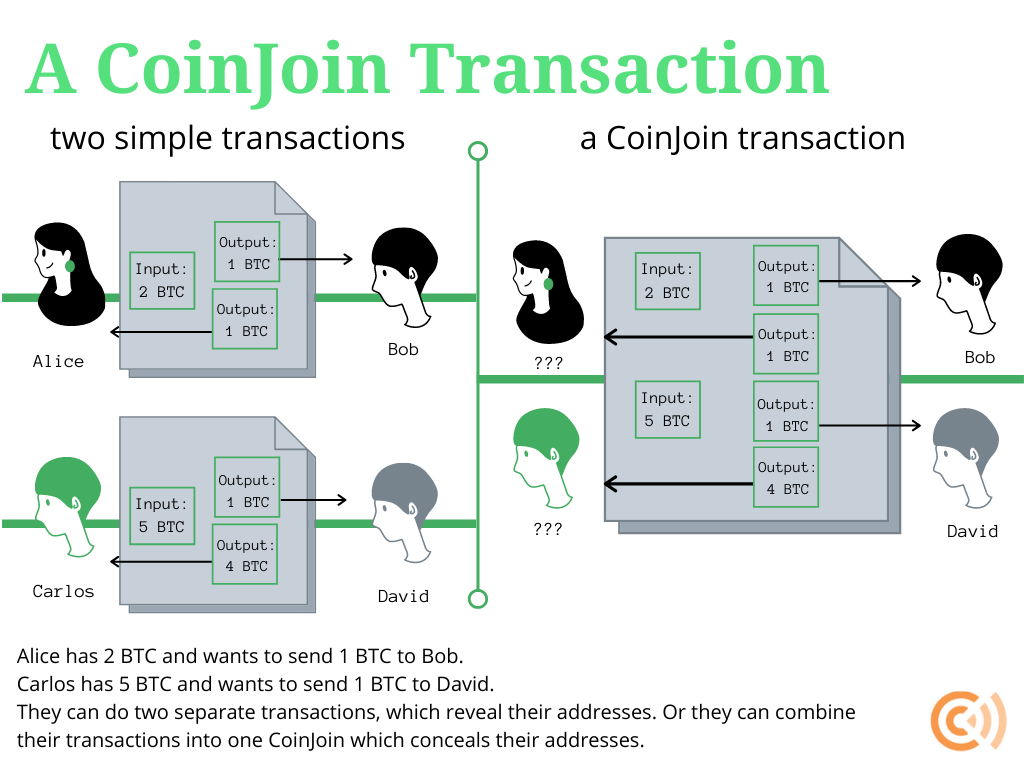

Bitcoin developers had been working on a non-custodial transaction privacy tool called CoinJoin since 2013. With a CoinJoin transaction, two or more senders combine their inputs to be sent to two or more output recipients. The inputs sum to the amount of the outputs, yet an observer looking at the blockchain would not be able to easily tell any address, sender identity, or sum involved. Even the recipient of a CoinJoin transaction could not tell the sender’s address just looking at the blockchain. Recipient addresses, however, would be viewable on the blockchain.

Today, CoinJoin functionality is offered by popular wallet software. CoinJoin transactions were first offered by the Dark Wallet alpha release in 2014. Today, wallets like Wasabi and Samourai offer CoinJoin options to users. Importantly, CoinJoins operate on a non-custodial basis. It is simply a Bitcoin transaction type that individual users can initiate, not a service that requires a third party to control keys or coins.

One limitation of CoinJoin transactions is that they require users to coordinate to send the transaction at the same time. Wallet software provided by Wasabi and Samourai—particularly Samourai’s recent Whirlpool application—helps to alleviate this problem somewhat by making it easier for users to initiate CoinJoins, but users may still have to wait to find others to join in the transaction. Although Wasabi and Samourai software makes it easier for their users to initiate CoinJoins, neither service provider acts as a custodian. At no point do Wasabi and Samourai wallet developers have control of user keys.

A special CoinJoin application called JoinMarket overcomes this problem by allowing users to pre-pay for a CoinJoin. Users who don’t mind waiting to make a transaction, called market-makers, collect fees from users who would like to quickly make a payment, called market-takers. At no point does any party have complete control over transaction funds—JoinMarkets are non-custodial.

A developing variant of a CoinJoin, called a CoinSwap, may overcome the limitations of recipient vulnerability and equal-input requirements. In a CoinSwap, users send coins to a multi-signature address—or a wallet that requires signatures from some majority of n private keys in order to move funds—that are withdrawn on the other side from the wallets of the other users. A special cryptographic trick called a hash-time-locked contract prevents any party from stealing funds. The key benefit of a CoinSwap is that the transaction looks like a simple transaction on the blockchain, when in reality, the parties to a CoinSwap concealed the senders and recipients addresses from the blockchain. Privacy-preserving wallet services like Wasabi are already examining how they can integrate CoinSwap functionality in their software.

Privacy-preserving cryptocurrencies

The optional privacy-preserving Bitcoin tools described above improve on the general lack of privacy with simple Bitcoin transactions. However, they may still leave some kind of trace, limited though it may be, on the blockchain if they are not perfectly executed. They are also complex and sometimes cumbersome to use, so less technical users may find it difficult to adequately wield them.

Furthermore, since these tools are not the default mode of interacting with the bitcoin blockchain, some worry that using them may draw unwarranted attention from third parties and law enforcement. For example, third party exchanges may block or track transactions that they believe have come from a privacy technique like a CoinJoin transaction. This would be a problem from Bitcoin fungibility, since certain coins would be less marketable than others. Additionally, without privacy by default, innocent non-technical users who are unfamiliar with their options may be denied privacy protections that should, arguably, automatically protect all.

For these reasons, some developers have endeavored to create cryptocurrencies that implement privacy techniques at the protocol level. These “privacy-preserving cryptocurrencies,” or “privacycoins,” are separate from Bitcoin. They are peer-to-peer blockchain-based cryptocurrencies, but they operate in special ways to conceal senders, recipients, or amounts, or some combination thereof, from third parties.

One of the reasons that cryptocurrencies like Bitcoin are radically transparent is that it allows anyone to view the blockchain and verify that transactions are accurate. In other words, there is a tradeoff between privacy and authentication. Custom built privacy-preserving cryptocurrencies endeavor to build a technological way to provide both privacy and authentication.

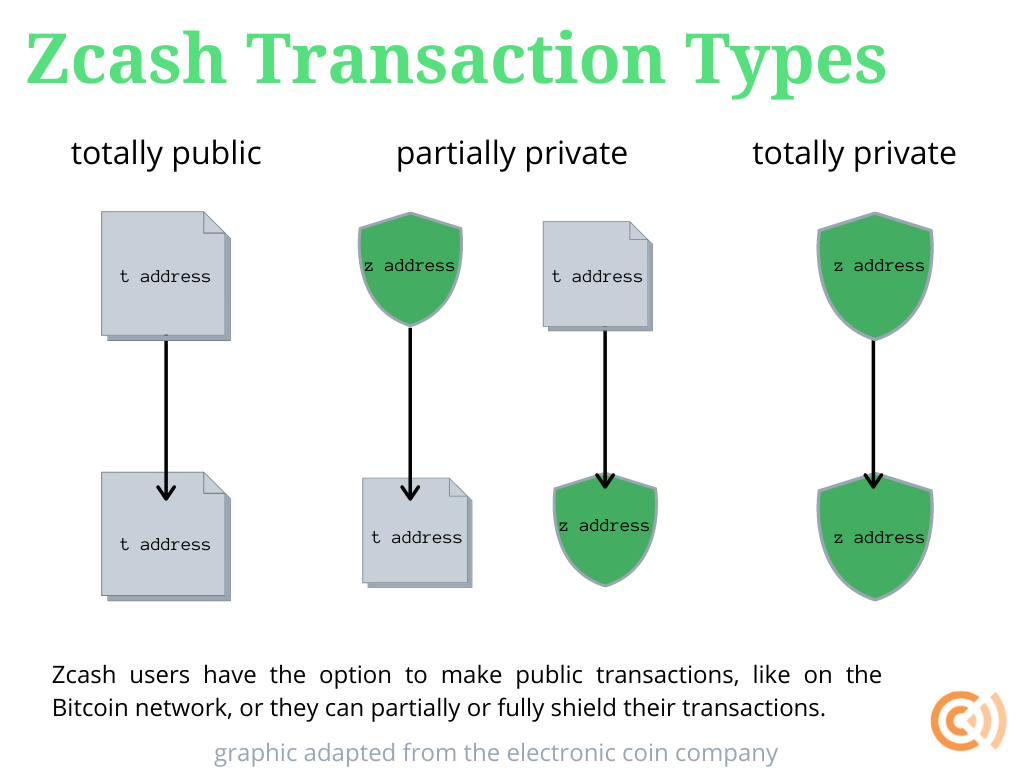

One of the oldest privacy-preserving cryptocurrencies is Zcash, born in 2016 from earlier academic research projects, Zerocoin and Zerocash. Like Bitcoin, Zcash is peer-to-peer cryptocurrency with a supply limit of 21 million that is maintained and validated by an open network of miners. But Zcash can afford greater privacy at the protocol level through the application of what are called zk-SNARKs, or “zero-knowledge Succinct Non-Interactive arguments of Knowledge.” In a nutshell, Zcash gives users the default option to transact using a public address, just like a Bitcoin address, or a private “shielded” address, which is hidden yet verifiable on the blockchain using zk-SNARKs.

A zero-knowledge proof is a mathematical technique for one party to prove to another that a statement is true without revealing anything other than the validity of the statement itself. When applied to Zcash, the proof in question is that a given transaction is valid.

Zcash’s bleeding-edge use of zk-SNARKs has been characterized as “so mind-bending it seems taken from the pages of a science fiction novel.” Although uniquely innovative and developed by well-known cryptographers, shielded transactions still constitute a minority of all Zcash activity compared with fully transparent transactions: as of May of 2020, only 6 percent of Zcash transactions were fully shielded (meaning a shielded address sent money to another shielded address) while 15 percent were partially shielded (meaning a transparent address sent money to a shielded address or vice versa).

Shielded transactions can also be accompanied by an encrypted memo field to convey transaction details—otherwise kept private—to relevant parties; shielded transaction details can also be made visible to third parties or the public at large by sharing a “view key” that’s otherwise kept private by senders and recipients. Though novel and complicated, Zcash provides one compelling option for cryptocurrency users seeking enhanced privacy.

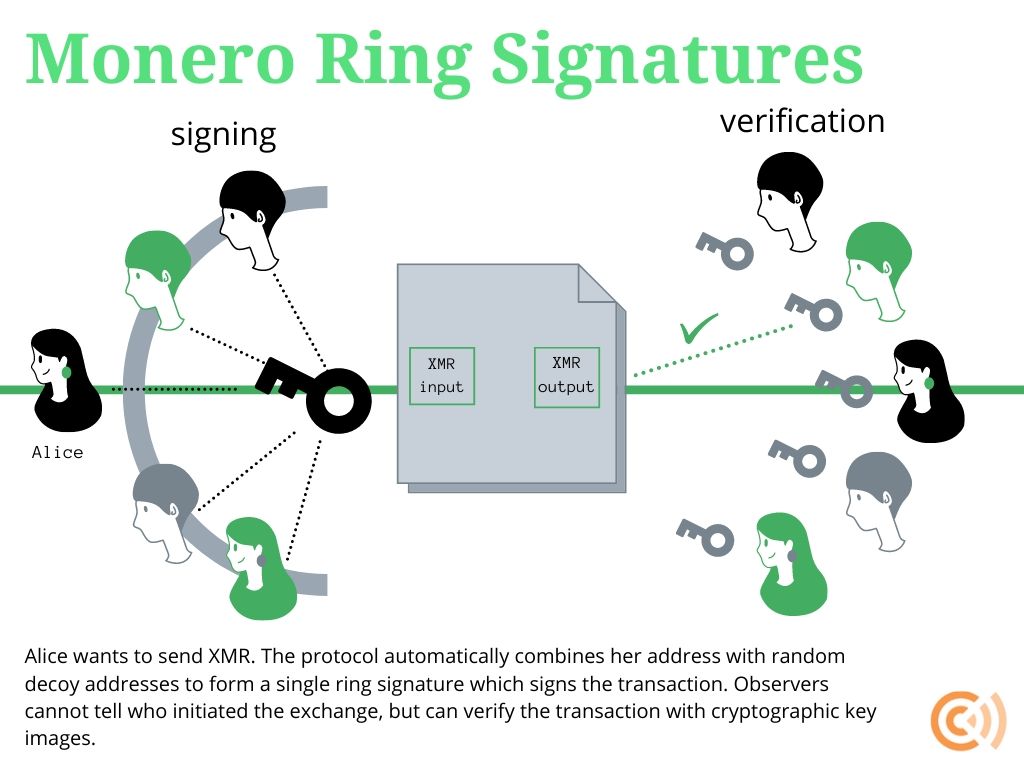

Another popular privacy-preserving cryptocurrency is called Monero, from the Esperanto word for money. With Monero, all senders, recipients, and amounts are concealed by default, but users have the option to share certain information with intended recipients if they desire. This is why the Monero project describes itself as “private by default and optionally semi-transparent.”

Monero preserves the privacy of senders through what is called a ring signature. When a Monero user broadcasts a transaction, their personal signature is combined into a group of other Monero users’ signatures so that an observer cannot tell which signature actually produced the initiating signature. Every Monero transaction is structured this way by default, so no user draws attention to themselves by choosing whether or not to use ring signatures.

A special kind of ring signature, called ring confidential transactions or RingCT, conceals transaction amounts in Monero. RingCT was implemented in January 2017 and is now mandatory for all network transactions. Just like ring signatures and zero-knowledge proofs, the “multi-layered linkable spontaneous anonymous group signature” or MLSAG at the core of RingCT conceals private data while allowing observers to verify that transactions are authentic with special encryption techniques. RingCTs are also non-custodial and do not require full third-party control of coins.

A final default privacy tool on Monero is called a stealth address, which conceals recipients. Each user has a public address that is 95 characters and starts with a 4. But whenever someone sends money to a public address, it is actually sent to an auto-generated stealth address that no unrelated observer can see. Monero users have the option to reveal their transactions and account balances if they would like if they choose to reveal their private view key. But Monero transactions are structured to be automatically private by default.

As with Bitcoin and Zcash, Monero presents certain weaknesses. For instance, questions surround Monero’s auditability. Bitcoin’s radical transparency presents challenges for privacy, but it makes technologically auditing individual entities and the total currency supply trivially easy. Monero’s default privacy makes such auditing more difficult; for example, an undiscovered bug could inflate the Monero money supply in a way that is hard to detect. (Still, inflation bugs have also occurred with public blockchain cryptocurrencies like Bitcoin and hybrid cryptocurrencies like Zcash.) Monero developers acknowledge this limitation and urge users to evaluate their own risk preferences involved with the privacy/auditability tradeoff. (Shielded Zcash transactions present a similar auditability problem.)

Zcash and Monero are just two privacy-preserving cryptocurrencies. We have highlighted these two to contrast two different approaches and describe some of the tools they use. Other examples include Mimblewimble implementations like Grin and Beam (which use confidential transactions techniques) and Komodo (which is a fork of Zcash).

Use cases and implications

It is true that privacy-preserving technologies and cryptocurrencies may be used for unwanted activities, just as it is true that cash may be used in such ways. But there are many socially beneficial uses of privacy-preserving technologies and cryptocurrencies that far outweigh the minority of undesired uses. Besides, the right to privacy is a core component of living in an open society.

For example, privacy-preservation techniques improve individual security. Let’s say a business accepts cryptocurrency and amasses a small fortune in their public address. A criminal viewing the blockchain could find that business to be an irresistible target. She could break into the business, hold a gun to someone’s head, and demand the private keys to steal the money. Using privacy technologies can make a business less vulnerable to such attacks.

Or consider someone who does not wish to have their behavior scrutinized and influenced, like through advertisements targeted based on previous purchases. If a person’s wallet is linked to their identity, marketing agencies can analyze their transactions to try to track them across the web and sell them goods and services. Using privacy techniques shields users from ad tracking.

There are more prosaic applications of privacy technology. Let’s say someone wants to get their tech-savvy spouse a surprise gift for their birthday without it being tracked on their shared accounts. A sneaky wife may check her husband’s cryptocurrency wallet to try to get an idea of her gift. Privacy tools help preserve the joy of a holiday secret.

More fundamentally, the right to privacy is a foundational part of the open society. Free peoples may decide what to share or conceal from the public. It is a human right, and it is one that is now available with digital purchases thanks to privacy-preserving cryptocurrency tools. A globally accessible list of all citizen’s transactions may be a boon to law enforcement but it is also a disaster for pro-democracy agitants living under oppressive totalitarian regimes.

Fortunately for policymakers, the legal implications of these technologies are similarly clear. Privacy techniques that involve third party control of funds and keys, such as centralized mixer services, are subject to surveillance regulations intended for custodial services. Techniques and cryptocurrencies that do not involve third party control of funds and keys, such as CoinJoins, Zcash, and Monero, are not subject to such regulations but, again, custodial entities within those ecosystems, e.g. an exchange that sells consumers a privacy protecting cryptocurrency, are.

The Financial Crimes Enforcement Network of the US Treasury Department (FinCEN), the top federal money-laundering watchdog organization in the US, has issued clear rules on which cryptocurrency entities are subject to financial regulations that distinguish custodial from non-custodial applications, exempting the latter. Specifically, mere users, software developers, miners, and multi-signature wallet transactions involved with privacy-preserving cryptocurrency techniques are non-custodial and therefore exempt. Custodial parties, such as centralized mixers, are not exempt.

Cryptocurrency industry, and consequently the decentralized finance space, have evolved beyond what many initially thought possible. What’s more, a growing number of hedge fund managers, institutional investors, and governments have given the green flag for crypto to thrive. With that said, many are yet to realize cryptocurrency and DeFi’s full potential. Although Bitcoin is hitting the headlines, understanding how to make a passive income with DeFi is often seen as a complex, high-risk endeavor. Read on for an easily understood breakdown of how to make a passive income with decentralized finance!

In this article, we look at some of the most important considerations for deciding how to make a passive income with DeFi. Also, we’ll explore some of the various methods of generating passive income streams and the projects facilitating the DeFi revolution. As such, we touch on some of the most popular DeFi projects, such as UniSwap, Compound, Balancer and much more.

What Is Decentralized Finance?

To begin with, let’s answer the basic question of “what is decentralized finance”. Decentralized finance (DeFi) is the term used to categorize a broad range of financial applications that utilize cryptocurrency and blockchain technology. DeFi is posed to disrupt traditional financial intermediaries by removing middle-men from financial transactions.

.

In many ways, human intermediaries, or gatekeepers, have been a burden on financial transactions for many years. While the traditional financial system is fractured and highly inefficient. DeFi allows for value transfer across several complex financial instruments. Crucially, this occurs even with the absence of centralized entities such as legacy banks, and consequently without the control of a single organization or party. This gives users of DeFi greater levels of control and financial freedom. Before the buzzword “DeFi” came about, “Open Finance” was an umbrella term used to describe many of the features within DeFi.

Some of the most common applications in DeFi include lending, decentralized exchanges (DEXs), staking, derivatives, crowdfunding, and insurance. All of these services are made available in DeFi without the need for third-party intermediaries. Instead, DeFi applications are highly automated, and largely rely on smart contracts. You can interact directly with smart contracts to execute trades, token swaps, and much more.

Decentralized Finance on Ethereum

The majority of DeFi applications are built on the Ethereum blockchain, the second-largest cryptocurrency platform. Despite this, however, several other blockchains are emerging that could compete with the DeFi offerings made available by Ethereum. In particular, Cardano, EOS, and Polkadot are platforms that are pushing DeFi both outside of Ethereum, and in a way creating interoperability with Ethereum.

However, there are many good reasons that the majority of DeFi has been built on Ethereum. Ethereum has created a platform that is based around programmable money. As opposed to Bitcoin, which is oftentimes referred to as “digital gold”, Ethereum is the technological solution to the unease felt in traditional financial markets. As the global financial infrastructure is in a state of flux, DeFi is reshaping the global economic landscape by bringing permissionless, borderless, open finance to the masses.

The appeal of DeFi is further compounded by the effects of the COVID-19 coronavirus pandemic. On a worldwide scale, interest rates are flirting with negative returns. Furthermore, unprecedented stimulus packages are devaluing the underlying fundamentals of almost every major fiat currency. DeFi offers a lifeline to those that may have previously been excluded from basic financial services, by offering the same financial tools that are available to everyone.

Why is DeFi So Popular?

Globally, DeFi has created tools for financial freedom. DeFi can be a useful tool for preserving wealth and avoiding harsh capital controls. Furthermore, DeFi platforms allow for fast and cost-efficient remittances outside of the traditional financial system, without KYC.

This is particularly useful for those without access to basic financial services, whether due to a lack of formal documentation, legal status, or because such services are not available locally. DeFi does not discriminate. DeFi promotes financial inclusion by providing access to financial instruments regardless of wealth, status, religion, or geography.

Another factor that makes DeFi so popular is the proliferation of stablecoins. Stablecoins provide a stable price-pegged asset on the blockchain that can be freely traded with other cryptocurrencies. One of the issues with stablecoins is that they are not always reliable. Some stablecoins use algorithms to keep the price as close as possible to $1. However, these valuations can fluctuate, and on occasion, can deviate drastically from their peg.

Stablecoins

Though this is infrequent, it can cause major problems for liquidity providers and yield farmers counting on that stablecoin remaining stable. Thanks to DeFi however, there are now a plethora of different stablecoins available. This means that many DeFi protocols can diversify by creating baskets of several different stablecoins to reduce the risk of such an event. Furthermore, stablecoins are providing the framework for various fintech and traditional banking firms to move into the crypto space.

DeFi also lowers the barrier of entry to participate in derivatives markets and synthetics. By using DeFi platforms like Synthetix, users can gain exposure to all kinds of markets without the need for a broker or other type of intermediary. Want to learn more about DeFi? Join +30,000 students already enrolled in Ivan on Tech Academy, and get 20% off with “BLOG20”.

DeFi For Everyone

Also, DeFi allows users to participate with much smaller investments than are required by many traditional services. As an example of how to earn a passive income with DeFi, an investor could gain access to the price of gold or stocks via the blockchain, without the need for a vault or a brokerage account.

DeFi has attracted the attention of many traditional traders. High yield and volatility are lacking in traditional markets. However, DeFi provides risk to suit every appetite. Trading altcoins is one of the highest-risk investment opportunities available in most markets. However, with correct risk management, trading altcoins can also be one of the most profitable forms of trading. Unsurprisingly, this is attracting attention from traders of all backgrounds. Perhaps one of the most captivating features of DeFi is wrapping services such as renBTC or Wrapped Bitcoin (WBTC).

These services allow Bitcoin hodlers to lock up their assets on an Ethereum protocol and mint ERC-20 tokens that are pegged to the price of Bitcoin. This has brought a wave of new users into the DeFi space. Wrapping services changed the minds of many Bitcoin maximalists about the value proposition of Ethereum. Also, wrapping services have added huge value to the DeFi space by putting idle BTC to work.

Prediction markets have become widely popular in the crypto space thanks to DeFi. The blockchain has created new markets that wouldn’t have otherwise been possible, introducing the concept of prediction markets to a new audience. With DeFi, you can bet on elections, sports, the weather, just about anything!

Although there are many exciting use cases for DeFi, many involve a high level of risk. One of the safest ways to understand the many benefits of this ever-evolving ecosystem is by learning how to earn a passive income with DeFi.

How To Earn A Passive Income With DeFi

UniSwap

One of the easiest ways to learn how to earn a passive income with DeFi is by becoming a Liquidity Provider (LP). Uniswap is a decentralized exchange whereby users can swap ERC-20 tokens directly from a web3 wallet to almost any other ERC-20 token. The key difference between DEXs such as Uniswap and centralized exchanges (CEXs) such as Coinbase and Binance, is that the tokens are made available by liquidity providers.

When making trades on CEXs, fees are paid to the exchange. However, with DEXs such as Uniswap, fees are paid to liquidity providers (LPs). LPs simply deposit an equal USD amount of two tokens, known as a pair, to a liquidity pool. Whenever these tokens are bought and sold, LPs earn a share of the fees generated by the token swaps.

For anyone hodling idle assets, wondering how to put them to work, providing liquidity to a platform like Uniswap is one of the simplest ways of understanding how to earn a passive income with DeFi.

Maker

Maker is one referred to as one of the founding fathers of DeFi. Considered by many to be the first building block on top of Ethereum, Maker was one of the major catalysts for the surge in DeFi adoption. MakerDAO is a decentralized autonomous organization that governs the Maker platform with the MKR token. Token holders can vote on updates to the protocol and events with the two Maker tokens generated, MKR and DAI.

Both the governance token MKR and the stablecoin DAI are ERC-20 tokens. DAI is one of the most popular stablecoins used by those who understand how to make a passive income with DeFi. Unlike stablecoins such as USDT or USDC, which rely on a centralized banking service backing the value of the coin, Maker approaches its stablecoin in a decentralized manner. The MKR token is burned in relation to any fluctuations in the DAI price, with holders incentivized to maintain the DAI token pegged to a $1 price.

The Maker platform offers borrowing and lending services, using smart contracts called Collateralized Debt Positions (CDP). Users can send their ETH to the Maker CDP smart contracts, to receive over-collateralized loans for up to 66% of the collateral value locked. DAI is the most-used decentralized stablecoin across the DeFi ecosystem. Using the Maker platform, you will soon learn how to earn a passive income with DeFi, using the DAI stablecoin in other DeFi applications.

Compound

Compound Finance is a decentralized, algorithmically-operated protocol for the lending and borrowing of cryptocurrencies. The Compound app comprises a sleek user interface and a visualization of the best interest rates for lending and borrowing.

Compound allows its users to borrow against their crypto collateral, or provide liquidity to the protocol. The interest rates for lending and borrowing are based on supply and demand. Compound has no lock-up period, meaning you are free to add or remove liquidity to pools frictionlessly.

As the name suggests, the idea is to earn interest that can be compounded by providing liquidity. Furthermore, users of the protocol earn the COMP governance token. The COMP token kickstarted the summer of DeFi. As the price of COMP increased dramatically, users began to realize the full potential of DeFi. Compound was catalytic in the birth of yield farming, whereby savvy liquidity providers jump from platform to platform in search of the highest yields possible.

Compound has already been audited and formally verified. Since May 2020, Compound has adopted community governance. Holders of the COMP token and their delegates debate, propose, and vote on all changes to Compound.

Aave

Previously known as ETHlend in the launch of November 2017, the peer-to-peer lending platform rebranded to Aave in January 2020. (Fun Fact: Aave is Finnish for Ghost). Aave is one of the most popular DeFi platforms for its ease of use and sleek interface. Additionally, Aave accepts a wide variety of assets and cryptocurrencies as collateral to use for loans. A bonus for users is being able to withdraw collateral at any time, with no mandatory lock-up period.

The protocol operates a bug bounty program – whereby developers are rewarded for finding any bugs or flaws within Aave’s infrastructure. On top of this, Aave has been through extensive auditing of their smart contracts. These security precautions and policies have radiated confidence to users, and in particular, the introduction of flash loans.

Flash loans are uncollateralized loans, that conduct all borrowing, lending, and repayment, all within the same transaction. For those new to the crypto industry, flash loans could be a very risky way to discover how to earn a passive income with DeFi. Do your own research, and make sure you understand the premise of a protocol before using it.

Balancer

The Balancer protocol was released in March 2020 on the Ethereum blockchain. Balancer is an automated market maker (AMM) that generates fees for liquidity providers. As a second layer platform built on top of Uniswap, Balancer allows AMMs to combine several assets into a single liquidity pool, even if they are unevenly weighted.

AMMs facilitate market-making without the need for intermediaries. Instead, algorithms determine the rules of any trades executed on the platform.

Balancer can be viewed as a type of self-balancing crypto ETF. Users can create and manage their own crypto index fund, or provide liquidity to an existing pool. These pools are self-balancing. This means that tokens can be freely exchanged without being removed from any given pool.

One of the key features of Balancer is its Constant Mean Market Maker (CMMM). This allows up to eight different tokens to enter a liquidity pool and be swapped or removed frictionlessly.

Yearn.Finance

Yearn Finance was developed single-handedly by Andre Cronje. The Yearn.finance protocol is a yield aggregator and DeFi ecosystem that maximizes yields for users of the platform. By using other DeFi protocols such as Curve, Aave, and Compound, Yearn.finance optimizes token lending and gives users the highest annual percentage yield (APY) available depending on their risk tolerance. This is done by locating the best returns for token lending across several platforms. All of this happens under the hood, saving a great deal of time and energy for users seeking optimal returns.

Among the various lending and farming opportunities proposed by Yearn.finance is the yPool on Curve finance. User deposits into the yPool are converted into “yield optimized tokens” (yTokens) including yUSDC, yUSDT, and yDAI. This function enables users to earn lending fees from Yearn but also trading fees from Curve. This is because liquidity is routed to various sectors of the DeFi space through yEarn.

Subsequently, Yearn has provided some of the most impressive rates of 2020. The platform is responsible for some of the largest gains made by yield farmers and is deemed by many to be one of the most innovative DeFi applications on the market. Yearn is also considered to be the most decentralized platform in DeFi.

Furthermore, thanks to its limited total supply of 30,000 YFI tokens, demand for the platform’s native token is substantial. In fact, the YFI token reached a staggering $43,000 during September and has shown remarkable strength since. At the time of writing, YFI is trading at $28,465 and has recovered considerably from its early November dump.

How To Earn A Passive Income With DeFi Summary

Decentralized finance is a great way to earn extra income, however, there are things to be wary of. Yield Farming protocols are sometimes referred to as ‘weird DeFi platforms’. Perhaps surprisingly, food meme coins like Yam, Pasta, and Sushi can sometimes offer substantial gains. More often than not, however, they are a one-way ticket to Rekt City. Protocols such as these require so much attention to price movement, that you could view this as more of an active, rather than passive income. Also, these projects are often short-lived and benefit only those who can get in early, before the inevitable post-launch dump.

Uniswap is a decentralized exchange protocol built on Ethereum. To be more precise, it is an automated liquidity protocol. There is no order book or any centralized party required to make trades. Uniswap allows users to trade without intermediaries, with a high degree of decentralization and censorship-resistance.

Uniswap is open-source software. You can check it out yourself on the Uniswap GitHub.

Uniswap works with a model that involves liquidity providers creating liquidity pools. This system provides a decentralized pricing mechanism that essentially smooths out order book depth. We’ll get into how it works in more detail. For now, just note that users can seamlessly swap between ERC-20 tokens without the need for an order book.

Since the Uniswap protocol is decentralized, there is no listing process. Essentially any ERC-20 token can be launched as long as there is a liquidity pool available for traders. As a result, Uniswap doesn’t charge any listing fees, either. In a sense, the Uniswap protocol acts as a kind of public good.

The Uniswap protocol was created by Hayden Adams in 2018. But the underlying technology that inspired its implementation was first described by Ethereum co-founder, Vitalik Buterin.

How does Uniswap work?

Uniswap leaves behind the traditional architecture of digital exchange in that it has no order book. It works with a design called Constant Product Market Maker, which is a variant of a model called Automated Market Maker (AMM).

Automated market makers are smart contracts that hold liquidity reserves (or liquidity pools) that traders can trade against. These reserves are funded by liquidity providers. Anyone can be a liquidity provider who deposits an equivalent value of two tokens in the pool. In return, traders pay a fee to the pool that is then distributed to liquidity providers according to their share of the pool. Let’s dive into how this works in more detail.

Liquidity providers create a market by depositing an equivalent value of two tokens. These can either be ETH and an ERC-20 token or two ERC-20 tokens. These pools are commonly made up of stablecoins such as DAI, USDC, or USDT, but this isn’t a requirement. In return, liquidity providers get “liquidity tokens,” which represent their share of the entire liquidity pool. These liquidity tokens can be redeemed for the share they represent in the pool.

So, let’s consider the ETH/USDT liquidity pool. We’ll call the ETH portion of the pool x and the USDT portion y. Uniswap takes these two quantities and multiplies them to calculate the total liquidity in the pool. Let’s call this k. The core idea behind Uniswap is that k must remain constant, meaning the total liquidity in the pool is constant. So, the formula for total liquidity in the pool is:

x * y = k

So, what happens when someone wants to make a trade?

Let’s say Alice buys 1 ETH for 300 USDT using the ETH/USDT liquidity pool. By doing that, she increases the USDT portion of the pool and decreases the ETH portion of the pool. This effectively means that the price of ETH goes up. Why? There is less ETH in the pool after the transaction, and we know that the total liquidity (k) must remain constant. This mechanism is what determines the pricing. Ultimately, the price paid for this ETH is based on how much a given trade shifts the ratio between x and y.

It’s worth noting that this model does not scale linearly. In effect, the larger the order is, the more it shifts the balance between x and y. This means that larger orders become exponentially more expensive compared to smaller orders, leading to larger and larger amounts of slippage. It also means that the larger a liquidity pool is, the easier it is to process large orders. Why? In that case, the shift between x and y is smaller.

What is impermanent loss?

As we’ve discussed, liquidity providers earn fees for providing liquidity to traders who can swap between tokens. Is there anything else liquidity providers should be aware of? Yes. There’s an effect called impermanent loss.

Let’s say that Alice deposits 1 ETH and 100 USDT in a Uniswap pool. Since the token pair needs to be of equivalent value, this means that the price of ETH is 100 USDT. At the same time, there’s a total of 10 ETH and 1,000 USDT in the pool – the rest funded by other liquidity providers just like Alice. This means that Alice has a 10% share of the pool. Our total liquidity (k), in this case, is 10,000.

What happens if the price of ETH increases to 400 USDT? Remember, the total liquidity in the pool has to remain constant. If ETH is now 400 USDT, that means that the ratio between how much ETH and how much USDT is in the pool has changed. As a matter of fact, there is 5 ETH and 2,000 USDT in the pool now. Why? Arbitrage traders will add USDT to the pool and remove ETH from it until the ratio reflects the accurate price. This is why it’s crucial to understand that k is constant.

So, Alice decides to withdraw her funds and gets 10% of the pool according to her share. As a result, she gets 0.5 ETH and 200 USDT, totaling 400 USDT. It seems like she made a nice profit. But hang on, what would have happened if she didn’t put her funds in the pool? She’d have 1 ETH and 100 USDT, totaling 500 USDT.

In fact, Alice would have been better off by HODLing rather than depositing into the Uniswap pool. In this case, the impermanent loss is essentially the opportunity cost of pooling a token that appreciates in price. This just means that by depositing funds into Uniswap in hopes of earning fees, Alice may lose out on other opportunities.

Note that this effect works regardless of what direction the price changes from the time of the deposit. What does this mean? If the price of ETH decreases compared to the time of the deposit, the losses may also be amplified. If you’d like to get a more technical explanation for this, check out Pintail’s article about it.

But why is the loss impermanent? If the price of the pooled tokens returns to the price when they were added to the pool, the effect is mitigated. Also, since liquidity providers earn fees, the loss may get balanced out over time. Even so, liquidity providers need to be aware of this before adding funds to a pool.

How does Uniswap make money?

It doesn’t. Uniswap is a decentralized protocol that doesn’t have a native token. All fees go to liquidity providers, and none of the founders get a cut from the trades that happen through the protocol.

Currently, the transaction fee paid out to liquidity providers is 0.3% per trade. By default, these are added to the liquidity pool, but liquidity providers can redeem them at any time. The fees are distributed according to each liquidity provider’s share of the pool.

A portion of fees may be dedicated to Uniswap development in the future. The Uniswap team has already deployed an improved version of the protocol called Uniswap v2.

1. Go to Uniswap

Install the Metamask wallet and purchase Ethereum if you haven’t done so already.

Then, visit Uniswap’s home page and click on “Launch App.” Though other Uniswap apps and frontends exist, beginners should first use the Uniswap official website.

2. Enter Swap Details

In the Uniswap app, enter the details of the trade that you want to make.

Enter the amount of cryptocurrency that you want to sell (1), the coin that you want to sell (2), and the coin that you want to buy (3).

Then, click “Swap” (4).

You can also configure other settings. If you set slippage tolerance and transaction deadlines, your transaction will be reversed under certain conditions.

Expert mode allows higher slippage limits.

3. Confirm the Trade on Uniswap

Confirm that the details of the swap are correct.

Next, confirm the details of the swap in your Metamask wallet. Enter a gas price and gas limit (1). Higher values will make your transaction go faster.

Then, click “Confirm” (2).

When the transaction has been submitted, close the window.

4. Check Your Transaction Status

You do not need to leave this window open for the transaction to continue. You can inspect it again in Metamask’s transaction history on a block explorer like Etherscan.

The fastest way to check your transaction is to click on your address in Uniswap’s toolbar (1) and then click on “View on Etherscan” (2).

5. Check Your Wallet

Once the transaction is complete, a new balance will show up in your Metamask wallet.

In this example, we traded ETH for DAI, which is shown at the bottom of the list as 115.348 DAI.

Part 2: Creating a Pool

1. Go to the Pool Page on Uniswap

As noted earlier, you can earn interest by depositing cryptocurrency in Uniswap’s liquidity pools. To do so, click on “Pool” in Uniswap’s main toolbar (1), then click on “Add Liquidity” (2).

2. Enter Pool Details

Enter the amount of cryptocurrency you want to deposit (1) and choose the coin you want to deposit (2). Then, choose a second coin for the other half of the trading pair you want to create (3).

In this example, we have created an ETH-to-DAI liquidity pool.

3. Approve the Transaction

Confirm the transaction in Metamask. You may need to reconnect your Metamask wallet if you have been offline for some time.

4. Wait For Your Deposit to Complete

Wait for Uniswap to approve your transaction. When other traders use your pool, you will earn interest. You can check the status of your pool on the Pool page.

If it does not show up, restore it by clicking on “Import” on Uniswap’s Pool page.

Part 3: Remove Your Stake

1. Go to the Pool Page on Uniswap

If you want to stop staking in a pool, you can withdraw your funds. First, go to the Pool page, find your pool, then click “Manage.”

Click “Remove” to proceed with the withdrawal. (Alternatively, you can add more funds to generate more income.)

2. Choose Withdrawal Amount

Choose the amount of funds that you want to remove by sliding the bar (1). In this example, we’ll remove all of the DAI we staked earlier.

Click “Approve” to continue (2).

(You can also withdraw your funds as a different cryptocurrency: click “Detailed” and choose another coin.)

In your Metamask wallet, sign the transaction.

3. Finalize the Withdrawal

Click “Remove” in Uniswap.

Click “Confirm” to finalize the withdrawal.

In Metamask, set your transaction fees (1) and click “Confirm.” (2)

4. Check Your Wallet

Your funds will arrive in your wallet.

Learn More About Uniswap

You can learn more about Uniswap by reading introduction to the platform. You’ll learn about its history, its features, the UNI token—and why it has become the most popular DEX on Ethereum.

Decentralized finance (commonly referred to as DeFi) is an experimental form of finance that does not rely on central financial intermediaries such as brokerages, exchanges, or banks, and instead utilizes smart contracts on blockchains, the most common being Ethereum. DeFi platforms allow people to lend or borrow funds from others, speculate on price movements on a range of assets using derivatives, trade cryptocurrencies, insure against risks, and earn interest in a savings-like account. Some DeFi applications promote high interest rates, with some providers offering triple-digit interest rates, but are subject to high risk. As of October 2020, over $11 billion was deposited in various decentralized finance protocols, which represents more than a tenfold growth during the course of 2020.

History

MakerDAO is credited with being the first DeFi platform. It launched in 2015 and allows people to take out loans of the stablecoin Dai and seeks to keep the price of Dai pegged to the U.S. dollar in a decentralized manner.

In June 2020, Compound Finance started rewarding lenders and borrowers of cryptocurrencies on its platform with, in addition to typical interest payments to lenders, units of a new cryptocurrency known as the COMP token, which is used for governance of Compound’s platform but is also tradeable on exchanges. Other platforms followed suit, launching the phenomenon known as “yield faming” or “liquidity mining,” where speculators actively shift cryptocurrency assets between different pools in a platform and between different platforms to maximize their total yield, which includes not only interest and fees but also the value of additional tokens received as rewards.

In July 2020, The Washington Post wrote a primer on decentralized finance including details on yield farming, returns on investments, and the risks involved. In September 2020, Bloomberg said that DeFi made up two-thirds of the cryptocurrency market in terms of price changes and that DeFi collateral levels had reached $9 billion.

DeFi revolves around applications known as DApps (decentralized applications) that perform financial functions on digital ledgers called blockchains, a technology that was invented for Bitcoin but has since caught on more broadly. Rather than transactions being with and through a centralised intermediary such as a cryptocurrency exchange, transactions are directly between participants, mediated by smart contract programs. DApps are typically accessed through a Web3 enabled browser extension or application, such as MetaMask. Many of these DApps can connect and work together to create complex financial services. For example, stablecoin holders can commit assets to a liquidity pool. Others can borrow from this pool, by contributing additional collateral, typically more than the amount of the loan. The protocol automatically adjusts interest rates based upon the moment-to-moment demand for the asset.

“Decentralization” refers to the lack of a central exchange. Smart contract programs for the DeFi protocols themselves are run using open source software by a community of developers and programmers.

One example of a DeFi protocol is Uniswap, which is a decentralized exchange or dex that runs on the Ethereum blockchain and allows for the trading of hundreds of different digital tokens that are issued on the Ethereum blockchain. Rather than relying on centralized market makers to fill orders, Uniswap’s algorithm incentivizes users to form liquidity pools for the tokens by issuing trade fees to those providing liquidity. A development team writes software for deployment on Uniswap, but the platform is ultimately governed by its users. Because no centralized party runs Uniswap, there is no one to check the identities of the people using the platform. It is not clear what position regulators will take on the legality of a platform like Uniswap.

Another example is “flash loans” which are uncollateralized loans of an arbitrary amount that are taken out and paid back within a single block interval, a duration of minutes or even seconds. While there can be legitimate uses for such loans, multiple exploits of DeFi platforms have used flash loans in short-term manipulation of cryptocurrency spot prices.

Criticism

Blockchain transactions are irreversible, which means that an incorrect transaction with a DeFi platform or even deployment of smart-contract code containing errors cannot always be easily corrected. Coding errors, and hacks, are common. In 2020, one platform known as Yam Finance quickly grew its deposits to $750 million before crashing days after launch due to a code error. Additionally, the code for the smart contracts that implement DeFi platforms is generally open-source software that can be easily copied to set up competing platforms, which creates instabilities as funds shift from platform to platform.

The person or entity behind a DeFi protocol may be unknown, and may disappear with investors’ money. Investor Michael Novogratz has described some DeFi protocols as “ponzi-like.”

Inexperienced investors are at particular risk of losing money using DeFi platforms due to the sophistication required to interact with such platforms and the lack of an intermediary with a customer-support department.

Ethereum is a decentralized, open-sourceblockchain featuring smart contract functionality. Ether (ETH) is the native cryptocurrency of the platform. It is the second-largest cryptocurrency by market capitalization, after Bitcoin.

Ethereum is the most actively used blockchain in the world.

Ethereum was proposed in 2013 by programmer Vitalik Buterin. Development was crowdfunded in 2014, and the network went live on 30 July 2015, with 72 million coins premined. The Ethereum Virtual Machine (EVM) can execute Turing-complete scripts and run decentralized applications. Ethereum is used for decentralized finance, and has been utilized for many initial coin offerings.

In 2016, a hacker exploited a flaw in a third-party project called The DAO and stole $50 million of Ether. As a result, the Ethereum community voted to hard fork the blockchain to reverse the theftand Ethereum Classic (ETC) continued as the original chain.

Ethereum is currently planning to implement a series of upgrades called Ethereum 2.0, which includes a transition to proof of stake and an increase in transaction throughput using sharding.

Ethereum was initially described in a white paper by Vitalik Buterin, a programmer and co-founder of Bitcoin Magazine, in late 2013 with a goal of building decentralized applications. Buterin argued that Bitcoin and blockchain technology could benefit from other applications besides money and needed a scripting language for application development that could lead to attaching real-world assets, such as stocks and property, to the blockchain. In 2013, Buterin briefly worked with eToro CEO Yoni Assia on the Colored Coins project and drafted its white paper outlining additional use cases for blockchain technology. However, after failing to gain agreement on how the project should proceed, he proposed the development of a new platform with a more general scripting language that would eventually become Ethereum.

Ethereum was announced at the North American Bitcoin Conference in Miami, in January 2014. During the same time as the conference, a group of people rented a house in Miami: Gavin Wood, Charles Hoskinson, and Anthony Di Iorio from Toronto who financed the project. Di Iorio invited friend Joseph Lubin, who invited reporter Morgen Peck, to bear witness. Six months later the founders met again in a house in Zug, Switzerland, where Buterin told the founders that the project would proceed as a non-profit. Hoskinson left the project at that time.

Ethereum has an unusually long list of founders. Anthony Di Iorio wrote: “Ethereum was founded by Vitalik Buterin, Myself, Charles Hoskinson, Mihai Alisie, & Amir Chetrit (the initial 5) in December 2013. Joseph Lubin, Gavin Wood, & Jeffrey Wilcke were added in early 2014 as founders.” Formal development of the software began in early 2014 through a Swiss company, Ethereum Switzerland GmbH (EthSuisse). The basic idea of putting executable smart contracts in the blockchain needed to be specified before the software could be implemented. This work was done by Gavin Wood, then the chief technology officer, in the Ethereum Yellow Paper that specified the Ethereum Virtual Machine. Subsequently, a Swiss non-profit foundation, the Ethereum Foundation (Stiftung Ethereum), was created as well. Development was funded by an online public crowdsale from July to August 2014, with the participants buying the Ethereum value token (Ether) with another digital currency, Bitcoin. While there was early praise for the technical innovations of Ethereum, questions were also raised about its security and scalability.

Binance makes it easy for anyone to buy Bitcoin (BTC). In this guide, we’ll walk you through the basics, so you can add crypto to your portfolio in minutes.

What is Bitcoin?

Bitcoin is the most popular and widely used cryptocurrency in the world.

Do I need to buy a whole Bitcoin?

Buying Bitcoin doesn’t have to be expensive. With Binance, you can buy a fraction of one Bitcoin from just $15.

Why choose Binance?

It’s the world’s largest crypto exchange trusted by millions of users worldwide. We make buying crypto fast, easy, and safe. 24/7 Customer Support team is always ready to help.

Ready to buy Bitcoin? Here are the steps:

If you’re an experienced crypto trader and want to open an account with Binance, sign up for a Binance account or download the Binance app. Otherwise, read this article for step-by-step instructions on how to buy Bitcoin with Binance.

Step 1: Create your Binance Account

Sign up with your email address or mobile phone number, and choose a strong password. Or, download the Binance crypto trading app from the App Store or Google Play store and open an account there.

Step 2: Start Buying Bitcoin

There are two main ways to buy Bitcoin on Binance: you can link your debit/credit card or bank account, or buy crypto directly from other users with P2P trades.

Linking your debit card, credit card, or bank account (available in select regions) is one of the easiest ways to buy Bitcoin. Head over to this page to get started: https://www.binance.com/en/creditcard.

Through this method, you can buy Bitcoin for a minimum of about 15 USD (amount varies depending on currency).

Buy Bitcoin directly from other Binance users with your local fiat currency. Browse a variety of Bitcoin listings to shop the best offers on Bitcoin from other users. In order to place an order, you must first deposit your local fiat currency to your Binance wallet.

{kind=link}